Paper 01

The Innovation–Adoption Paradox

Why a nation's capacity to invent AI does not predict its capacity to deploy it.

- Status

- Released

- Date

- Apr 19, 2026

- Reading

- 22 min

Abstract

The global economic landscape of early 2026 is defined by a contradiction: the frontier of AI innovation expands at unprecedented speed while the actual integration of AI into the workforce remains highly fragmented. This paper names that contradiction the Innovation–Adoption Paradox, locates it in the deployment gap between capability and absorption, and proposes four national archetypes, Adoption Leaders, Fast Movers, Regulated Adopters, and Stagnant Innovators, that managers can use to choose strategy.

00 / Listen

Audio companion to this paper.

00 / Paper

Introduction

The global economic landscape in early 2026 is defined by a profound contradiction that challenges traditional models of technological progress. While the frontier of artificial intelligence innovation expands at a rate previously unseen in industrial history, the actual integration of these capabilities into the functional core of the workforce remains highly fragmented. As Mejias (2026) observes regarding the deployment of transformative technologies:

“The benefits don't flow automatically to whoever develops them first. They flow to whoever deploys them most effectively across their workforce, their processes, and their communities.”

This phenomenon, referred to throughout the paper as the Innovation–Adoption Paradox, suggests that a nation's capacity to invent and develop sophisticated AI models does not inherently correlate with its ability to deploy those tools effectively across its economic sectors. As of the second half of 2025, approximately 16.3% of the world's population has used generative AI tools, yet the disparity between the Global North and the Global South, and between leading innovative hubs and rapid adoption leaders, continues to widen (Microsoft AI Economy Institute, 2026).

Artificial Intelligence as a General Purpose Technology

To understand the current diffusion landscape, AI must be analyzed through the historical lens of General Purpose Technologies (GPTs). Economists define a GPT as a technology that is pervasive across an economy, demonstrates continuous improvement over time, and spawns further innovation by making it easier to invent new products or processes (Bresnahan & Trajtenberg, 1995, as cited in Jovanovic & Rousseau, 2005). Only a handful of such technologies exist in human history, the steam engine, electricity, the computer, and the internet (Bashir & Sadowski, 2014).

The Mechanism of GPT Diffusion and the Productivity Paradox

The diffusion of a GPT rarely follows a linear path. Historical data on electricity and information technology shows that initial adoption often produces a temporary decrease in productivity, the phenomenon Robert Solow captured in 1987 when he noted the computer age was visible everywhere except in the productivity statistics (Bara, 2026). In 2026, the global economy is witnessing a return of the Solow Paradox in the context of AI. Azhar et al. (2025) define this paradox as a disconnect where the rapid progress and investment in AI technology fail to translate into greater social productivity and broad economic growth at the macroeconomic level. The disconnect is largely driven by the current deployment gap, which Bara (2026) defines as:

“The space between what a technology can do in isolation and what it does when embedded in actual workflows, approval chains, reporting structures, and organizational incentives.”

| GPT Era | Initial Productivity Response | Required Complementary Innovations | Long-term Impact |

|---|---|---|---|

| Electricity | Productivity slowdown (1890–1920) | Factory redesign, assembly lines, decentralized power | Massive 20th-century growth |

| Information Technology | Solow Paradox (1970–1990) | Process re-engineering, networked databases, digital literacy | The 1990s productivity boom |

| Artificial Intelligence | Deployment Gap (2023–2026) | Agentic workflows, sovereign infrastructure, institutional trust | Projected radical transformation |

The Compressed Diffusion Curve of Generative AI

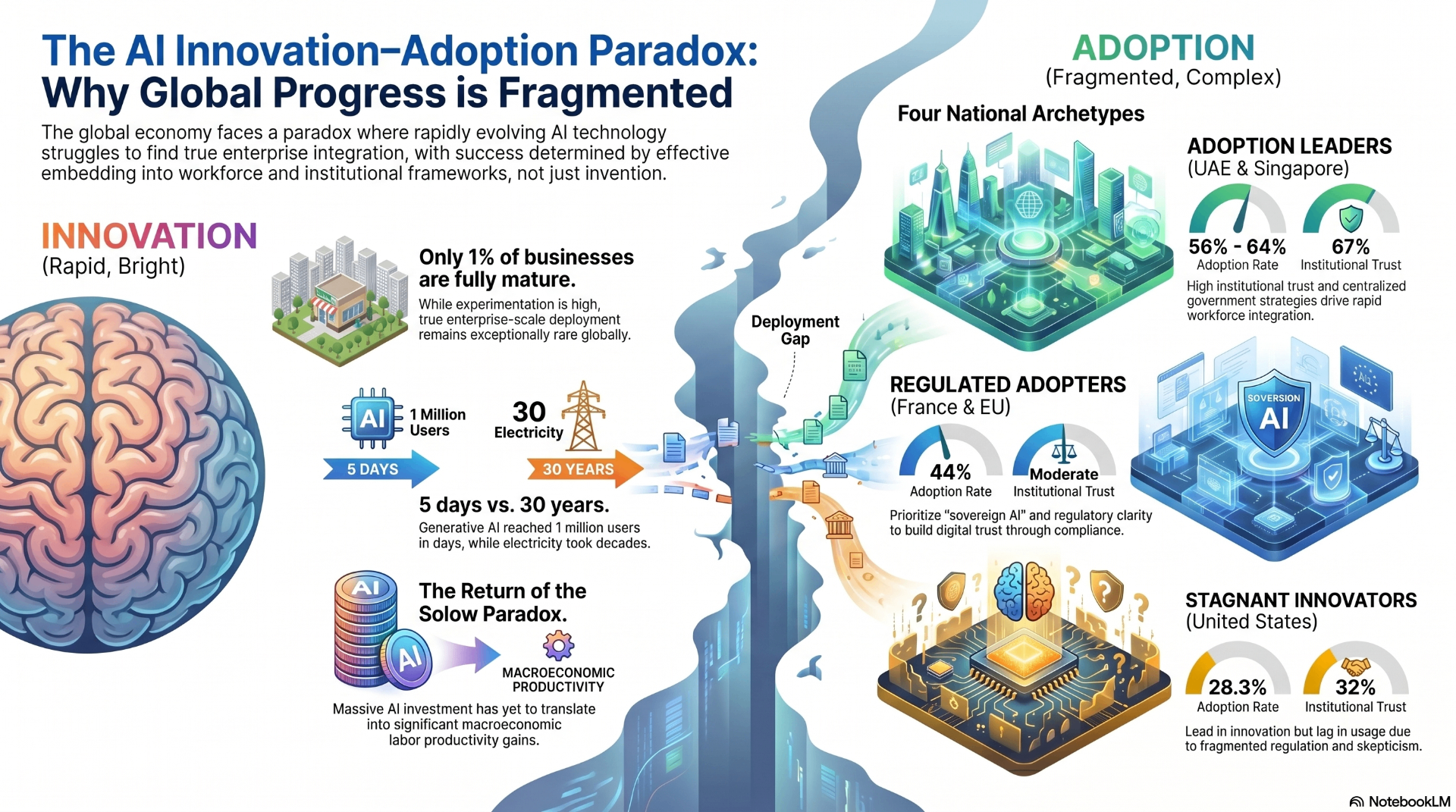

While historical GPTs required decades to permeate society, generative AI has spread at a highly accelerated pace (Machulla, 2025). To illustrate the contrast: while it took thirty years for early electrical grids to secure one million users, leading generative AI platforms achieved the same milestone in five days (Machulla, 2025). This extraordinary speed is fueled by the technology's viral nature, where the AI-generated output itself serves as an organic promotional tool that continuously draws in new users (Machulla, 2025).

However, this rapid consumer-level acceptance frequently obscures a severe implementation deficit within the business sector. Although experimentation is widespread and 40% of professional services firms report some degree of organization-wide usage (Thomson Reuters Institute, 2026), comprehensive integration remains exceptionally rare. Recent data shows an adoption rate of merely 6.9% among European SMEs (Segarra-Blasco et al., 2025, as cited in Sánchez et al., 2025), and a global assessment reveals that only 1% of businesses categorize their generative AI initiatives as fully mature (Tournesac et al., 2025).

Theoretical Frameworks for AI Diffusion

Analyzing the uneven spread of AI requires the integration of three foundational perspectives: the Diffusion of Innovations theory (Rogers, 2003), the Technology–Organization–Environment framework (Tornatzky & Fleischer, 1990), and Institutional Theory (DiMaggio & Powell, 1983; Meyer & Rowan, 1977). They are not competing explanations; they are complementary mechanisms operating at different scales.

Rogers' Diffusion of Innovations and the S-Curve

Rogers (2003) categorizes adopters into Innovators, Early Adopters, Early Majority, Late Majority, and Laggards. In the context of this paper, it is most useful not as a predictive model but as a classification mechanism for understanding how nations occupy different positions along the curve simultaneously. The rise of DeepSeek and other open-source platforms has eliminated traditional financial obstacles, allowing emerging economies to potentially leapfrog stages (Microsoft AI Economy Institute, 2026), what Machulla (2025) describes as a 'Big Bang' diffusion that challenges Rogers' classic predictability. National positions diverge accordingly: the United States exhibits Innovator characteristics, leading invention but lagging workforce adoption (Microsoft AI Economy Institute, 2026), while the UAE compresses the curve through centralized coordination (Mejias, 2026), and South Korea demonstrates leapfrogging via targeted investment in localized AI capabilities (Mejias, 2026; Microsoft AI Economy Institute, 2026).

The Technology–Organization–Environment Framework

TOE identifies three contexts that determine readiness: technological (data quality, infrastructure), organizational (leadership support, financial resources, workforce skills), and environmental (regulatory frameworks, industry competition, national strategies) (Sánchez et al., 2025). Research on Swedish SMEs highlights that AI adoption is shaped less by technical capability and more by organizational conditions and human judgment (Aljaraidah & Shihamit, 2026). Recent OECD data confirms the pattern: 52% of large firms used AI in 2025 versus only 17.4% of small firms, a readiness gap rooted in expertise, not access (OECD, 2026). These imbalances are visible across archetypes: Adoption Leaders such as the UAE align all three TOE dimensions through coordinated strategy (Digital Watch Observatory, 2024; Mejias, 2026); Regulated Adopters such as France pair strong environmental conditions with cautious organizational adoption (Introl, 2025; Oxford Insights, 2026); and Stagnant Innovators such as the United States combine high technological capability with weak organizational and environmental coherence (Mejias, 2026; Microsoft AI Economy Institute, 2026).

Institutional Theory and Isomorphism

DiMaggio and Powell (1983) identified three pressures that drive organizational conformity: coercive (regulatory mandates), normative (professional standards), and mimetic (imitating successful competitors). Mimetic pressure is doing extraordinary work in 2026, 91% of bank boards have now formally approved generative AI programs to keep pace with industry advancements (UXDA, 2025). Coercive pressure varies sharply by jurisdiction: while some governments implement strict legislative frameworks, the UAE has adopted regulatory pragmatism, using principles-based guidelines and sandbox environments to balance oversight with private-sector innovation (Microsoft AI Economy Institute, 2026).

Global Adoption Metrics and the Digital Divide

The 2025–2026 period has seen a widening divide in AI usage shares. While global adoption rose to 16.3% by the end of 2025, growth was concentrated in high-income, highly digitized economies (Microsoft AI Economy Institute, 2026).

| Region / Group | H1 2025 | H2 2025 | Growth |

|---|---|---|---|

| Global North | 22.9% | 24.7% | +1.8% |

| Global South | 13.1% | 14.1% | +1.0% |

| World Average | 15.1% | 16.3% | +1.2% |

| Students (16+) | — | 75.0% | High |

| Large Firms | — | 52.0% | High |

Note. Regional and global adoption shares adapted from Microsoft AI Economy Institute (2026); student and large-firm shares adapted from OECD (2026).

The divide is not merely geographic but demographic. The age gap in AI usage is staggering, 53.6 percentage points, with usage concentrated among students and those actively connected to the labor market (OECD, 2026). For managers, the workforce-level challenge is not a lack of interest but a readiness imbalance: younger workers are hyper-adopters while organizational leadership and infrastructure lag behind.

Archetype Analyses

The UAE: Adoption Leader

The UAE has navigated the paradox by establishing a centralized, government-led strategy that treats AI as a pillar of national economic diversification. Ranking #1 in AI diffusion by the end of 2025, it achieved a 64% usage rate among its working-age population (Microsoft AI Economy Institute, 2026). The UAE National Strategy for Artificial Intelligence 2031 frames the country as a test bed for AI solutions across energy, logistics, and healthcare, and the 'UAI' brand has attracted international talent (Digital Watch Observatory, 2024).

A critical differentiator is institutional trust. While only 32% of US residents trust AI, approximately 67% of UAE residents do (Edelman, 2025, as cited in Mejias, 2026), a trust built through visible, practical government adoption such as predictive traffic management and emergency-services routing (Mejias, 2026). To sustain it, leaders are adopting a glass-box governance posture: explainable AI tools, clear human accountability, and visible oversight (Grant Thornton, 2025).

South Korea: Fast Mover

South Korea provides the most compelling case of acceleration in 2025–2026, rising seven spots to 18th in global rankings (Mejias, 2026). The surge was driven by a $1 billion government investment in AI education and the development of localized 'Sovereign AI' tailored to Korean linguistic and cultural context (Mejias, 2026). Historically, English-centric LLMs have reflected predominantly North American norms and values (NAVER Cloud HyperCLOVA X Team, 2025), and major models consistently exhibit geographic bias against non-Western regions (Gopinadh et al., 2024). Naver's HyperCLOVA X dedicates roughly one-third of its pretraining data to Korean, and its Korean-optimized tokenizer requires less than half the tokens of GPT-4, vastly reducing inference cost compared to English-centric models (NAVER Cloud HyperCLOVA X Team, 2025).

France: Regulated Adopter

France has positioned itself as Europe's leading destination for AI investment by betting on 'sovereignty through the service layer' (Jahidi, 2026). Backed by €109 billion in investment, France aims to operate a low-carbon supercomputer deploying 500,000 GPUs by 2026 and 1 GW of compute capacity by 2028, powered by its decarbonized nuclear infrastructure (Crosley, 2026). In this context regulation functions as an accelerator, not a hindrance, EU AI Act compliance and domestic providers like Scaleway and OVHcloud anchor a sovereign-cloud ecosystem that keeps sensitive data under EU jurisdiction (Crosley, 2026; Jahidi, 2026; Introl, 2025; Oxford Insights, 2026).

The United States: Stagnant Innovator

The US leads the world in AI innovation and infrastructure, yet fell to 24th in workforce usage in 2025 (Microsoft AI Economy Institute, 2026). The primary headwind is a fragmented regulatory landscape, a sprawling federated system in which policy emerges asynchronously from countless state and federal entities (Mejias, 2026). Organizations must navigate a patchwork of state-specific rules such as the Colorado AI Act, Utah's AI Policy Act, and California's Transparency in Frontier AI Act (IAPP, 2026). Liability concerns compound the slowdown: 90% of organizations report that their privacy programs have expanded due to AI, yet 23% still lack a dedicated AI governance committee (Cisco Systems, Inc., 2026). A 2026 study of 500 companies found that only 14% possess a clear AI strategy, and 80% acknowledge that accountability for AI initiatives remains unclear (Koetsier, 2026).

The Return of the Solow Paradox

Evidence from 2025 confirms that AI demonstrably works at the task level, improving quality and speed for consultants and customer-service agents. But an NBER study found that 89% of managers saw no change in overall productivity between 2023 and 2026 (NBER, as cited in Bara, 2026). Daron Acemoglu calls this 'so-so automation', technology that substitutes labor to save costs but fails to radically improve underlying organizational processes (Acemoglu, as cited in Bara, 2026). Westmoreland (2026) describes the consequence as fragmentation debt: tools operating in isolation from the core business systems they were meant to transform. Lin et al. (2025) note that overcoming this deficit requires moving beyond technical deployment to achieve structural organizational AI readiness, and Azhar et al. (2025) confirm that shallow enterprise integration contributes directly to the AI Solow effect at the macroeconomic level.

Strategic Managerial Frameworks by Archetype

To move from pilot to profit, managers must shift their focus from the technological attributes of AI to the organizational and environmental factors that govern its success. Each archetype demands a different strategic posture.

1. The Ecosystem Integration Framework: for Adoption Leaders

- Behavioral shift, embed AI into high-visibility customer touchpoints; residents already accustomed to AI-powered government services expect the technology to feel familiar and useful (Digital Watch Observatory, 2024; Mejias, 2026).

- Regulatory alignment, move from black-box to glass-box governance with explainable AI, aligning with national KPIs (Grant Thornton, 2025).

- Competitive dynamics, leverage state-funded sovereign infrastructure and integrate with national digital initiatives like the 'UAI' brand (Digital Watch Observatory, 2024).

2. The Cultural Optimization Framework: for Fast Movers

- Behavioral shift, recognize that customers prioritize culturally relevant interactions; default global LLMs amplify systemic inequities (Gopinadh et al., 2024), while Sovereign AI such as HyperCLOVA X provides cultural resonance global competitors cannot match (NAVER Cloud HyperCLOVA X Team, 2025).

- Regulatory alignment, partner with domestic tech giants to keep enterprise data culturally and linguistically contextualized in response to sovereign initiatives like South Korea's AI Basic Act (Microsoft AI Economy Institute, 2026).

- Competitive dynamics, exploit speed-to-market and lower inference cost from locally optimized tokenizers, which require less than half the tokens of English-centric LLMs (NAVER Cloud HyperCLOVA X Team, 2025).

3. The Trust-Through-Compliance Framework: for Regulated Adopters

- Behavioral shift, pivot marketing to emphasize sovereign cloud ecosystems perceived as safe, localized, and GDPR-compliant (Crosley, 2026).

- Regulatory alignment, treat EU AI Act compliance as a strategic differentiator, not a legal cost (Tournesac et al., 2025), and use domestic providers like Scaleway or OVHcloud to keep data under EU jurisdiction (Crosley, 2026; Jahidi, 2026).

- Competitive dynamics, leverage decarbonized national infrastructure such as France's nuclear-powered supercomputers for sustainable, low-carbon AI operations (Crosley, 2026; Tournesac et al., 2025).

4. The Accountability & Risk Framework: for Stagnant Innovators

- Behavioral shift, invest in human-in-the-loop workflows; 64% of US workers expect AI to lead to fewer jobs over the next two decades (Stanford HAI, 2026).

- Regulatory alignment, build a robust legal-compliance desk capable of managing state-level liability hurdles (IAPP, 2026) and stand up dedicated AI governance committees (Cisco Systems, Inc., 2026).

- Competitive dynamics, winners will not be those with the best models but those that first solve the accountability gap with clear executive ownership and rigorous ROI tracking (Bara, 2026; Koetsier, 2026; Westmoreland, 2026).

MNE Cross-Country Operational Framework

For multinational enterprises navigating these archetypes, the one-size-fits-all approach is obsolete. MNEs should adopt a Polycentric AI Governance Model:

- Localized compute strategy, execute data-heavy training within Regulated Adopter hubs that offer decarbonized sovereign infrastructure (Crosley, 2026).

- Cultural layering, deploy local LLM architectures or wrappers in Fast Mover markets to align with regional linguistic and cultural nuance (NAVER Cloud HyperCLOVA X Team, 2025).

- Global ethical core, maintain a unified glass-box governance standard across all regions to satisfy Regulated Adopters and earn institutional trust in Adoption Leader markets (Grant Thornton, 2025).

Country examples by archetype (2025–2026)

| Country | Adoption rate (2025) | Institutional trust index |

|---|---|---|

| Singapore | 66% | 63% |

| United Arab Emirates | 56% | 67% |

Note. Adoption data adapted from Cybernews (2026); Visual Capitalist reports Singapore slightly lower at 60.9% (Neufeld, 2026). UAE trust index adapted from the Edelman Trust Barometer via Neufeld (2026) and Mejias (2026); Singapore trust index adapted from Stanford HAI (2026).

| Country | YoY adoption growth | Current adoption |

|---|---|---|

| Pakistan | +300% | 12% |

| India | +267% | 11% |

| Japan | +183% | 17% |

| South Korea | >80% | 30.7% |

Note. Pakistan, India, and Japan adapted from Cybernews (2026); South Korea adapted from Microsoft AI Economy Institute (2026) and Mejias (2026).

| Country | Adoption rate (2025) |

|---|---|

| Norway | 46.4% |

| Ireland | 44.6% |

| France | 44.0% |

Note. Adoption rates adapted from Visual Capitalist (Neufeld, 2026).

| Country | Adoption rate (2025) | Institutional trust index |

|---|---|---|

| United States | 28.3% | 32.0% |

Note. U.S. adoption rate adapted from Visual Capitalist (Neufeld, 2026); U.S. trust index adapted from the Edelman Trust Barometer via Neufeld (2026) and Mejias (2026).

Conclusions and Recommendations

The Innovation–Adoption Paradox of 2026 confirms that a nation's capacity for AI invention does not guarantee economic integration. The transition of AI into a mature General Purpose Technology is stalled not by technical limitations but by a lack of organizational readiness and institutional trust (Bara, 2026; Lin et al., 2025). Resolving the Solow Paradox requires managers to pivot from task-level experimentation toward systematic maturity, synchronizing deployment with the environmental and organizational contexts defined by the four national archetypes (Azhar et al., 2025; Sánchez et al., 2025).

To overcome these barriers, leadership must solve the accountability gap by establishing formal ownership structures that move AI beyond the opaque black box and into a transparent glass-box governance framework (Grant Thornton, 2025; Koetsier, 2026). In Adoption Leader and Fast Mover contexts, success depends on aligning corporate strategy with national sovereign-AI initiatives (Mejias, 2026; NAVER Cloud HyperCLOVA X Team, 2025). In Regulated Adopter and Stagnant Innovator environments, practitioners must navigate fragmented legal landscapes and prioritize data sovereignty (Cisco Systems, Inc., 2026; IAPP, 2026; Stanford HAI, 2026).

For multinational enterprises, the path forward lies in a polycentric operational model that balances localized cultural layering with a centralized ethical core (Crosley, 2026; NAVER Cloud HyperCLOVA X Team, 2025). Ultimately, the organizations that bridge the paradox will be those that view AI integration as a fundamental transformation of institutional identity rather than a mere technological upgrade. By aligning the TOE framework with archetype-specific strategies, managers can convert the current implementation deficit into a sustainable engine for global productivity.

01 / Why I explored this

I kept watching the same gap widen between countries inventing AI and countries actually absorbing it into work. The vendor narrative blamed access. The numbers told a different story, about institutions, trust, and deployment. This paper is my attempt to name that gap structurally rather than rhetorically.

02 / The question I was wrestling with

When the technology is held constant across borders, what determines whether a country's workforce actually absorbs AI, and what does that mean for the managers operating inside those countries?

03 / Key insights

- 01

AI is a General Purpose Technology, and every prior GPT, electricity, IT, produced a multi-decade productivity lag before payoff. The Solow Paradox is back, dressed as the 'deployment gap.'

- 02

Generative AI's diffusion curve is compressed beyond historical comparison: 5 days to a million users versus 30 years for early electrical grids. That speed hides a severe enterprise implementation deficit, only ~1% of firms call their generative AI initiatives mature.

- 03

National outcomes split into recognizable archetypes: Stagnant Innovators (the US, invents fastest, deploys unevenly), Centralized Accelerators (the UAE, 64% workforce usage via state coordination), Fast Movers (South Korea), and Constrained Adopters across much of the Global South.

- 04

No single theory explains the spread. Rogers' Diffusion of Innovations, the Technology–Organization–Environment framework, and Institutional Theory have to be stacked, adopters, organizations, and the rules around them all move on different clocks.

- 05

For managers, the binding constraint is institutional, not technical. Executive ownership, ROI tracking, and the trust infrastructure surrounding the system beat raw model access in every archetype studied.

05 / Visual summary

A 2×2 of national position (Innovator ↔ Adopter) against institutional readiness, with the four archetypes plotted and the deployment gap shaded as the region between capability and absorption.

06 / Citations

35 citations▸

- Aljaraidah & Shihamit, 2026

Aljaraidah, S., & Shihamit, E. (2026). Technological, organisational and environmental factors affecting AI adoption: Insights from leaders and employees in Swedish SMEs [Master's thesis, Uppsala University]. DiVA Portal.link

- Azhar et al., 2025

Azhar, S., Zhang, Z. X., & Lu, S. Y. (2025). Empirical analysis of the Solow paradox in artificial intelligence. Open Journal of Business and Management, 13(5), 3716–3729.link

- Bara, 2026

Bara, M. (2026, February 15). The AI productivity paradox is not a paradox. It is a pattern. Medium.link

- Bashir & Sadowski, 2014

Bashir, S., & Sadowski, B. M. (2014, June 22–25). General purpose technologies: A survey, a critique and future research directions [Conference presentation]. 25th European Regional Conference of the International Telecommunications Society (ITS), Brussels, Belgium.link

- Bresnahan & Trajtenberg, 1995

Bresnahan, T. F., & Trajtenberg, M. (1995). General purpose technologies: 'Engines of growth'? Journal of Econometrics, 65(1), 83–108. (As cited in Jovanovic & Rousseau, 2005.)

- Cisco Systems, Inc., 2026

Cisco Systems, Inc. (2026). Cisco 2026 data and privacy benchmark study.link

- Crosley, 2026

Crosley, B. (2026). France's AI sovereignty push. Introl.link

- Cybernews, 2026

Cybernews. (2026, February). AI adoption index 2025: Which countries use AI tools the most?link

- Digital Watch Observatory, 2024

Digital Watch Observatory. (2024). The UAE national strategy for artificial intelligence 2031.link

- DiMaggio & Powell, 1983

DiMaggio, P. J., & Powell, W. W. (1983). The iron cage revisited: Institutional isomorphism and collective rationality in organizational fields. American Sociological Review, 48(2), 147–160.

- Edelman, 2025

Edelman. (2025). Edelman Trust Barometer. (As cited in Mejias, 2026.)

- Gopinadh et al., 2024

Gopinadh, M. P. V. S., Sindhu, K. L., Raju, S. S. P. R., & Swarna, Y. (2024). Regional bias in large language models. arXiv.link

- Grant Thornton, 2025

Grant Thornton. (2025). Transition from 'black box' to 'glass box': The AI governance framework for UAE leaders.link

- IAPP, 2026

International Association of Privacy Professionals. (2026, February 4). Global AI law and policy tracker.link

- Introl, 2025

Introl. (2025). France's AI sovereignty push: Infrastructure behind the European AI champion.link

- Jahidi, 2026

Jahidi, A. (2026, March 3). Where global economies sit in the AI stack. Franklin Templeton.link

- Jovanovic & Rousseau, 2005

Jovanovic, B., & Rousseau, P. L. (2005). General purpose technologies (NBER Working Paper No. 11093). National Bureau of Economic Research.link

- Koetsier, 2026

Koetsier, J. (2026, April 8). AI transformation: No one's at the wheel, says 500-company study. Forbes.link

- Lin et al., 2025

Lin, B., Yang, Q., & Wang, X. (2025). AI adoption in business decision-making: Challenges, enablers, and organizational readiness assessment. International Journal of Social Science and Education Research, 8(11), 253–257.link

- Machulla, 2025

Machulla, P. (2025, January 8). The compressed diffusion curve: How generative AI redefines innovation adoption. Medium.link

- Mejias, 2026

Mejias, M. (2026, January 27). What the UAE and South Korea know about AI adoption that American organizations don't. Sidecar AI.link

- Meyer & Rowan, 1977

Meyer, J. W., & Rowan, B. (1977). Institutionalized organizations: Formal structure as myth and ceremony. American Journal of Sociology, 83(2), 340–363.

- Microsoft AI Economy Institute, 2026

Microsoft AI Economy Institute. (2026, January). Global AI adoption in 2025 – AI Economy Institute.link

- NAVER Cloud HyperCLOVA X Team, 2025

NAVER Cloud HyperCLOVA X Team. (2025). HyperCLOVA X THINK technical report. arXiv.link

- Neufeld, 2026

Neufeld, D. (2026, January 22). Mapped: AI adoption rates by country. Visual Capitalist.link

- OECD, 2026

Organisation for Economic Co-operation and Development. (2026). OECD digital education outlook 2026. OECD Publishing.link

- Oxford Insights, 2026

Oxford Insights. (2026). AI in France: Betting on AI adoption and sovereignty rather than racing for the most powerful models.link

- Rogers, 2003

Rogers, E. M. (2003). Diffusion of innovations (5th ed.). Free Press.

- Sánchez et al., 2025

Sánchez, E., Calderón, R., & Herrera, F. (2025). Artificial intelligence adoption in SMEs: Survey based on TOE–DOI framework. Applied Sciences, 15(12), 6465.link

- Stanford HAI, 2026

Stanford Institute for Human-Centered Artificial Intelligence. (2026). AI index report 2026: Public opinion.link

- Thomson Reuters Institute, 2026

Thomson Reuters Institute. (2026). 2026 AI in professional services report.link

- Tornatzky & Fleischer, 1990

Tornatzky, L. G., & Fleischer, M. (1990). The processes of technological innovation. Lexington Books.

- Tournesac et al., 2025

Tournesac, A., Hjartar, K., Krawina, M., Hillenbrand, P., & Olanrewaju, T. (2025). Accelerating Europe's AI adoption: The role of sovereign AI capabilities. McKinsey & Company.link

- UXDA, 2025

UXDA. (2025). Financial AI in practice: 21 case studies of artificial intelligence in banking CX.link

- Westmoreland, 2026

Westmoreland, H. (2026, April 7). What the 2026 Thomson Reuters AI in professional services report reveals for tax and audit firms. Certinia.link

08 / Future questions

- — Can the UAE's centralized model be transplanted, or is it inseparable from the political structure that produced it?

- — What does the Stagnant Innovator pattern look like at the firm level, not just the national one?

- — At what point does compressed diffusion stop rewarding fast followers and start punishing them?

End of paper 01